We have seen that to keep pace with increasing competition, companies are always going in for new ideas implemented through new projects be it for expansion, diversification or modernization. A project is an activity that involves investing a sum of money now in anticipation of benefits spread over a period of time in the future.

Put differently, we have assumed that: the value of one rupee now – Value of one rupee at the end of 2 years and so on. We know intuitively that this assumption is incorrect because money has time value. How we define this time value of money and build it into the cash flows of a project? The answer to this question forms the subject matter of this chapter.

We intuitively know that Rs.2000 on hand no is more valuable than Rs.2000 receivable after a year. In other words, we will not part with Rs.2000 now in return for a firm assurance that the same sum will be repaid after a year.

This additional compensation required for parting with Rs.2000 now is called ‘interest’ or the time value of money normally, interest is expressed in terms of percentage per annum e.g. 14 percent p.a or 16 percentage p.a and so on.

Money can be employed productively to generate real returns. For example, if a sum of 1000 invested in raw material and labor results in finished goods worth Rs.1050 we can say that the investment Rs1000 has earned a rate of return of 5 percent.

In today a rupees today have higher purchasing power than a rupee in the future.

Nominal or market interest rate

The = Real rate of interest or return

+Expected rate of inflation

+Risk premiums to compensate for uncertainty

Example

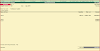

If A has a sum Rs.2000 to be invested, and there are two schemes, one offering a rate of interest of 10 percent, compounded annually, and other offering a simple rate of interest 10 percent, which on should opt of for assuming that he will withdraw at the end of a) one year b)two years and c)five years?

Solution

End of year

|

Compoud interest Scheme

|

Simple Interest Sch TIME VALUE OF MONEY

|

1

|

2000 + (2000*0.10)=2200

|

2000 + (2000*0.10)=2200

|

2

|

2200 + (2200*0.10)=2420

|

2200 + (2000*0.10)=2400

|

3

|

2420 + (2420*0.10)=2662

|

2400 + (2000*0.10)=2600

|

4

|

2662 + (2662*0.10)=2928.2

|

2600 + (2000*0.10)=2800

|

5

|

2928.2+(2928.2*0.10)=3221

|

2800 + (2000*0.10)=3000

|

From this table, it is clear that under the compound interest scheme interest earns interest, whereas interest does not earn any additional interest under the simple interest scheme.

Obviously, an investor seeking to maximize returns will opt for the compound interest scheme if his holding period is more than a year.

Future value of a lump sum (Single Flow)

The above table illustrates the process of determining the future value of a lump sum amount invested at one point in time.

FVn = PV(1+k)n

Where

FVn = Future Value of the initial Flow n years hence

PV = initial cash flow

K = Annual rate of interest

N = Life of investment

The fixed deposit scheme of SBI bank for example

Period of Deposit

|

Rate per Annum

|

46 days to 179 days

|

7%

|

180 days to < 1 year

|

8%

|

1 year and above

|

11%

|

An amount of RS 10000 invested today will grow in 3 years to

|

|

FVn = PV (1+k)n

|

|

=10000(1+0.11)3

|

|

=10000(1.368)

|

|

=RS.13680

|

|

Growth Rate

The compound rate of growth for a given series a period of time can be calculated by employing the future value interest factor table (FAVIF)

FVn=PV(1+K/M)MN

Continuous to Read click Investment and Capital Structure Decision

Click on link below to Read interesting topic English and Hindi

· नीचे दिए गए लिंक पर क्लिक करें पढ़ें दिलचस्प विषय अंग्रेजी और हिंदी

· What is GST in India? Goods & Services Tax Law Explained

· भारत में GST क्या है? माल और सेवा कर कानून समझाया

· What is Gratuity How to calculate? Is Income Tax Exempted on Gratuity?

· ग्रेच्युटी क्या है? गणना कैसे करें? क्या ग्रेच्युटी पर आयकर छूट है?

Continuous to Read click Investment and Capital Structure Decision

{kind=link}

0 Comments